How often should PA declarations be sent and how can duplicates be avoided?

The regulatory frequency depends on the VAT regime.

| VAT regime | Frequency | Deadline days |

|---|---|---|

| Monthly normal actual regime | e-reporting transaction data by ten-day periods | 20th of the same month for the first ten-day period, 30th of the same month for the second, 10th of the following month for the third |

| Quarterly normal actual regime | Monthly transmission | Before the 10th of the following month |

| Simplified VAT regime | Transaction data and, when they exist, monthly payment data | Between the 25th and 30th of the following month |

| VAT exemption threshold | Transaction data and, when they exist, bimonthly payment data | Between the 25th and 30th of the month following the end of the two-month period |

For February, the second deadline of the monthly normal actual regime is naturally adapted to the end of the month. These days correspond to the deadlines indicated by the French tax administration in the official e-reporting transmission frequency and deadline table. Payment data deadlines therefore do not mean that all payments must be declared: they concern collections for operations whose VAT is due on collection.

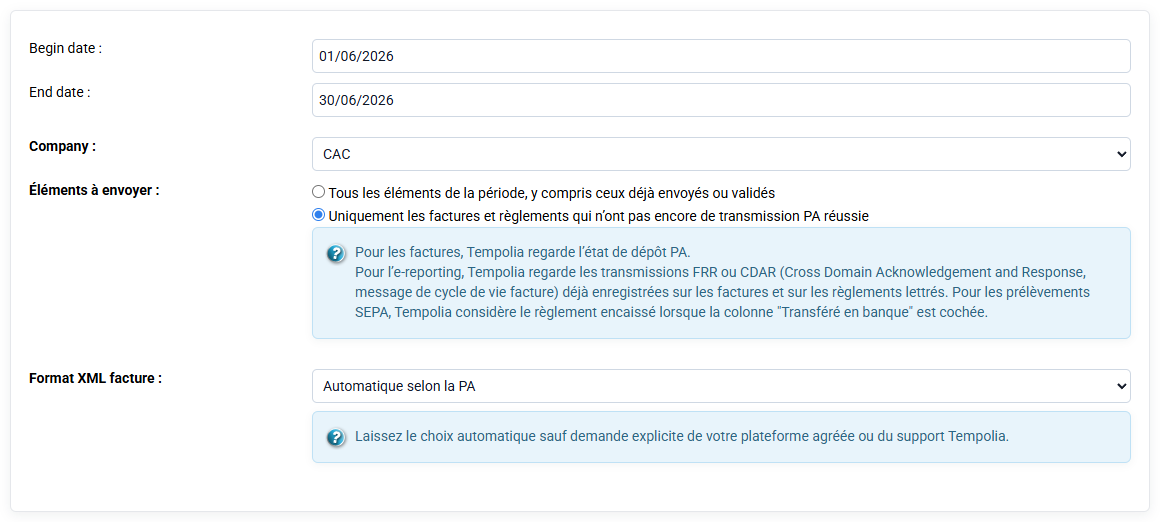

The PA may accept more frequent deposits, but Tempolia keeps track of what has already been sent. In the PA form, the differential option sends only invoices and payments that are not already validated as transmitted. This option is recommended for periodic processing because it avoids redeclaring a payment that has already been sent.

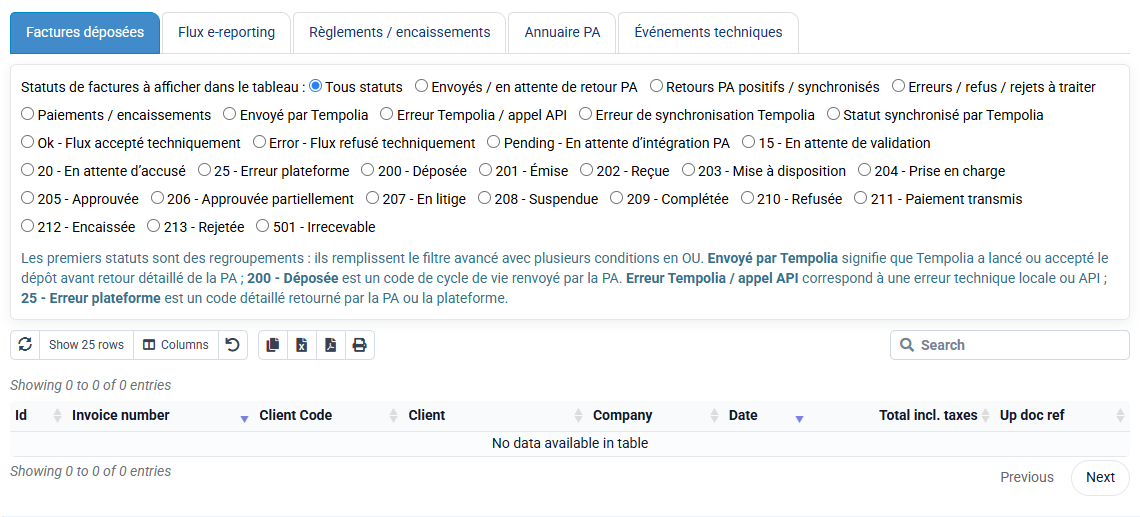

If an error occurred, consult PA history before relaunching. A line in error can be corrected and sent again. A line already sent and then corrected must be analyzed with its history. In that case, do not simply delete the trace: understand the event, create a negative corrective payment if necessary, then transmit the expected items to the PA used.